Michelle Martinelli Patton at Linkorp wrote this article for Mondaq.

The Panamanian Government with the aim of improving the competitiveness of the international services industry in Panama and, at the same time, comply with international standards for the effective exchange of information, initiated in 2009 a decisive agenda for the selection of countries with whom tax agreements were going to be negotiated.

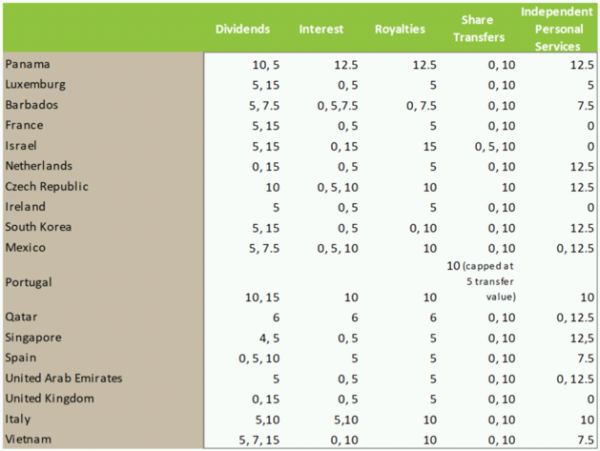

To date Panama has seventeen DTA in force with Mexico, Barbados, Qatar, Spain, Luxembourg, Netherlands, Singapore, France, South Korea, Portugal, Ireland, Czech Republic, Unit Arab Emirates, United Kingdom, Israel, Italy and Vietnam; that basically recognize reduce tax rates or the non-application of withholding taxes for certain type of income, such as royalties, interest, dividend and services.

Per Panama tax regulations the application of treaty benefits is recognized through the submission of an application by the Panamanian withholding agent to the Revenue Office, along with specific information and other documentation on the recipient of the income with the object of demonstrating that the recipient satisfies what is expressly stated in the article of the applicable treaty. Panama Tax Authorities will examine the application and issue a decision as to whether treaty benefits will be granted. A negative response will generate the payment of withholding tax per domestic rates, plus surcharges and late interest payments.

Under Panama’s domestic law the following withholding tax rules applies:

- Dividends are subject to a 10% dividend tax when paid out of domestic profits; the rate drops to 5% when the dividends are paid out of foreign-source or export profits, or out of certain income (e.g. interest from government bonds and capital gains derived from the sale of such bonds and interest on bank deposits)

- Interest is subject to a 12.5% withholding tax.

- Royalties are subject to a 12.5% withholding tax.

- Capital Gains on the sale or transfer of capital or securities economically invested in Panama, either directly or indirectly, are subject to a fixed rate of tax of 10%. Nonetheless, the buyer will always be required to withhold from payment and remit to Tax Authorities an amount equal to 5% on the aggregate proceeds of the sale, as an advance payment of the capital gain tax. The transfer of other assets is subject to a 10% capital gain tax.

- Independent personal services. Withholding tax will apply if payments relate to services rendered within or outside Panama regarding a taxable income-generating activity. Withholding tax rate is of 12.5% for companies, and when rendered by an individual applicable tax rates will be those related to natural persons on 50% of the amount invoiced.

The following table show a comparison of benefits under Panama’s domestic law as compared to the treatment under the tax treaties that are currently in force:

* Applicable tax rate may differ from treaty rates (e.g. lower rate/exemption under domestic law). Specific conditions will have to be observed to benefit of a reduce rate or the non-application of withholding taxes.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

Contact Michelle Martinelli Patton

About the Author